Select online apps from the list at the right. You’ll find everything you need to conduct business with us.

isolved People Cloud

QuickBooks Online

QuickBooks Desktop

Bill

Zoom

Your business needs more than tax prep—you need a team that helps you plan ahead, reduce your tax burden, and make smart financial decisions.

Sarah Johnson

Timothy McAdams D.D.S.

Vernon Smith

and less paperwork

on your numbers

in charting the future of your business

Keep your finances organized with accurate, up-to-date records.

Minimize your tax burden with year-round planning and compliance.

Ensure your team gets paid on time, every time, without the hassle.

Understand how your business is performing with expert reporting and strategic guidance.

Starting, running, and growing a business takes more than just keeping the books in order. We help with bookkeeping, tax planning, payroll, and accounting so you start with a solid financial foundation.

We’re with you all year, not just at tax time.

We understand the local economy & seasonal shifts of Cape Cod.

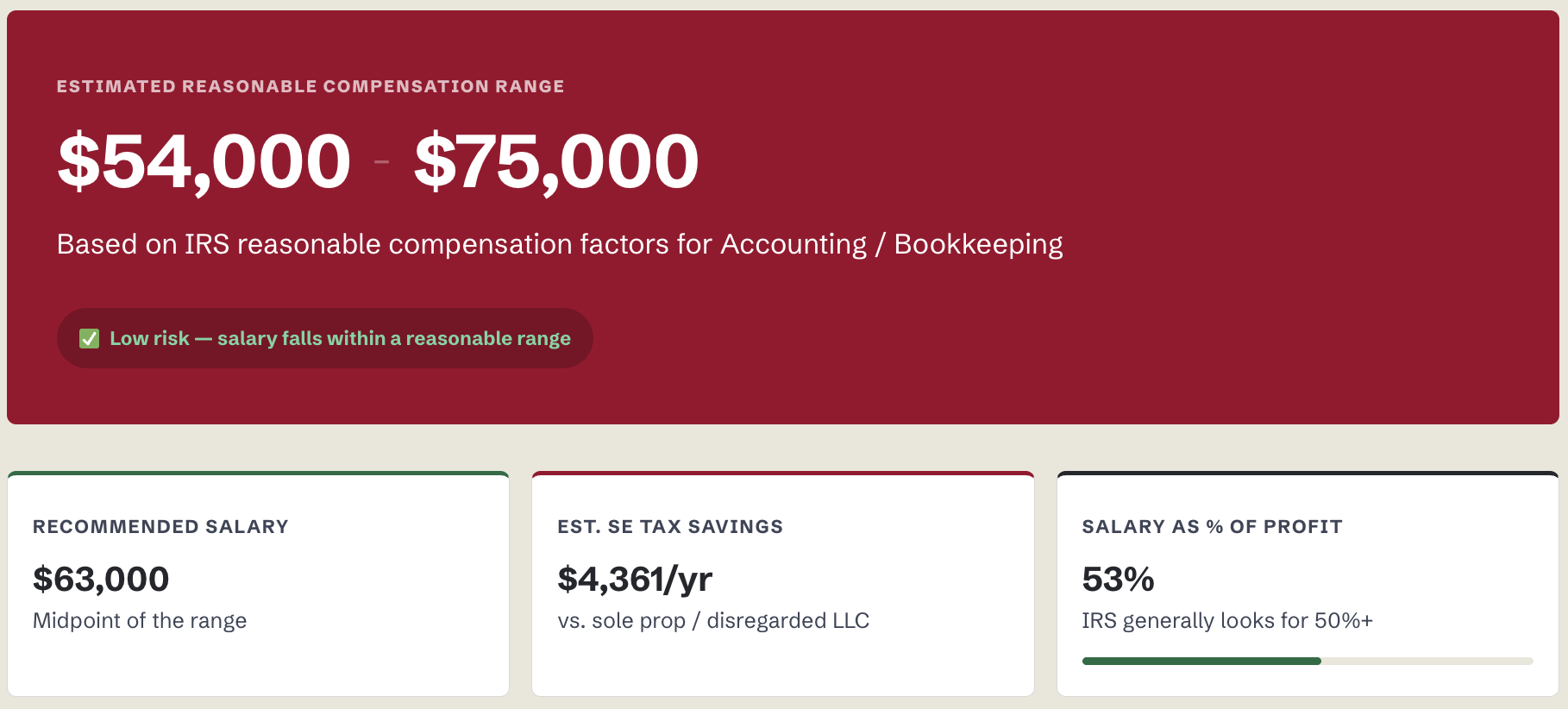

Try the calculator for free.